In our office, we have been discussing how to implement effective design cost control and/or monitoring. We have had the good fortune to have worked on many different levels of projects from multi-billion dollar high-performance jet program to much more humble part 23 prototypes. We have learned the importance of asking the following questions: Why use a NAS or MS bolt when AN bolt will do?, what is the true cost delta of a weldment vs a CNC machining? a metal fabrication vs a CNC machining? What cost driver triggers the move to composite materials? Which composite material offers the best cost/performance compromise?

The answer, as always, is “it depends”. It depends on the number of parts to be made/procured, it depends on the tolerances required, the strength requirements, supply chain security, the in-house skills available vs using an outside contractor, does the company quality system have the facility to support your choice? The relative cost impact on certification of the available choices, the cost of labor, etc etc

There are universally acknowledged cost drivers – the cost/weight trade off, the idea that at a certain point weight reduction means the introduction of additional complexity and therefore cost – although a few years ago I was sat in a meeting with a leading aircraft company president and he denied that the cost/weight relationship existed. “Universally acknowledged” may be an overstatement…..

Regardless, most designers and analysts have a vague notion of whether something is more expensive than something else. On occasion, if they design something particularly egregious the manufacturing engineer will send them a nasty email about how expensive it is going to be.

On a part by part basis and on a sub-assembly basis engineers are used to tracking part count and weight in the Bill of Material – either on the face of the drawing or in a separate material and weight accounting system. One thing we have never seen (please let us know if this is done at any organizations we have not worked with) is a cost column included on the bill of material that the engineer creates. Typically, the engineer is blind to the unit cost of each of the items.

Engineering is a discipline that should and does include cost control, whether or not the engineer realizes it. Product development means developing a product that can be sold at a competitive price point and make a profit. Engineers generally do not deal with cost on as regular basis as they deal with strength, weight, durability – but they should have an intimate understanding of cost. We have noticed a lack of cost consciousness in ourselves and with the projects we work with – and in some cases, our cost consciousness has been improved through significant cost constraints placed on projects by our clients.

So what cost goes on the drawing? – the cost of a prototype part can be many times the cost of a production part and the numbers involved in an initial production run may be many times lower than the number of parts produced in the overall life of the product.

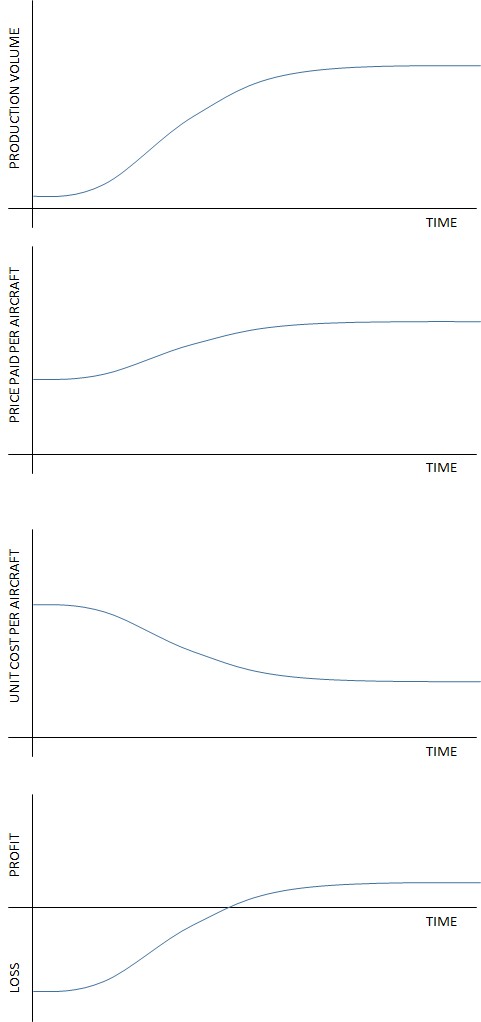

The most egregious example of this is the development of the Eclipse aircraft program where the final price point of the aircraft was predicated on the assumption that they would sell 1000 aircraft per year. While optimism is a very important aspect of getting a new product or company off the ground, an excess of optimism creates an excess of ‘undesirable outcomes’. The costing done in Eclipse was likely unrealistic even if they had reached their desired production rate.

This is especially critical if the program tends to run beyond the intended schedule. The first aircraft orders placed are at the initial offering price. The price of the aircraft tends to increase over time as reality bites. If the development schedule extends this problem is worsened because there are additional development costs to recoup in addition to the basic (and increasing) manufacturing cost. There are many aircraft that were initially offered to the market at sub $1M prices that end up at over $2M.

The effect of this on the OEM can be catastrophic. After the expensive development process has been completed an OEM often has to face the harsh reality of selling the first year or more of aircraft at a loss. The initial customers end up paying less than the cost of manufacture of the aircraft.

This often will drive a company into bankruptcy a few months into serial production. Just when you think they should be beginning to reap the benefits of the many years of expensive development, the financial backers have to dig deeper and sometimes this is too much for the corporation.

Understanding the true cost of the aircraft and how the cost changes during development may not avoid this issue but it will put companies in a position of

- Controlling the cost, or at the very least having visibility of the cost

- Being able to plan to cope with the first few months or years of production and work with the investors to manage expectations and keep the company solvent

I know that many larger companies do understand these issues and manage them effectively. For smaller aircraft companies it often looks like these issues are either unexpected or mismanaged in some way. This is understandable, smaller companies have a smaller talent pool and less experience to draw on within the management team. There is

a greater probability that some issues will fall through the cracks and this issue seems to be one that has proven fatal for many companies and aircraft programs.

In smaller aircraft companies there is a need for all staff to be multi-disciplined some extent. It is time that engineering started to pay more attention to the critical commercial aspects of the work they do and help management by making better choices and communicating the kind of commercial information that allows management to improve planning and make better decisions. It is common for engineering to blame management for commercial failures.

Including detailed cost breakdowns in the data produced and used by engineering will be useful only if the information is realistic. Realistic costing helps in two major ways.

- an accurate absolute cost per unit lets the corporation set a realistic price point and understand the margin on the finished product vs the sale price- and all of point 2. below

- an accurate relative cost per unit lets the product development team make rational choices between alternatives and understand what is driving cost into the product but does not help set the price point or calculate the profit margin.

I suggest that unit cost for the realistic production rate is put in the Bill of Material and on the drawing. A realistic production rate will be a bone of contention. It is not just Eclipse that is guilty of blue-sky thinking in that arena.

For low volume production, an approximate relationship between the volume ordered and the difference in cost should be established and used to estimate the higher cost per

aircraft.

To conclude – should we regard cost control like weight control? We spend the extra time to get the last gram or ounce out of part – should we do the same to get the last cent, penny or rupee out of a part? Is an aircraft that has great performance and payload capacity but no profit margin any better or worse than an aircraft that fails to meet its performance marks but can be made at a profit?

Comment On This Post